Piling On

When we were kids, we played a game…well, it wasn’t actually a game, it was just a thing we did, where someone would shout out “Dog Pile” and someone else would jump on the ground and then everyone else would start piling on top of them. Laughing bodies stacked on top of laughing bodies. As the number of bodies started to pile up, it became a lot less fun for those on the bottom of the pile, and eventually the laughter became a little bit manic and the person on the very bottom would scream for everyone else to get off. The bodies would quickly unstack themselves amidst a lot of pushing and pulling and, inevitably, we were back on our feet and ready for the next game. Looking back, it is a wonder we survived our childhoods.

Recently, it felt a little bit like someone yelled “Dog Pile”. Maybe it was Covid, or maybe it was Putin, or it might have been Inflation, or Stagflation, or Reflation, or a Bomb Cyclone Hurricane (whatever that is) but somebody yelled something and it felt like we were at the bottom of the pile. Inflation is the highest it has been since the early 1980s, the housing market is on a tear, there are supply shortages around the globe, energy prices are climbing, mortgages just topped 5% and the Fed is eyeing several more rate increases this year.

Yet, unemployment is at historic lows, consumer sentiment is on the rise, household spending is up and we are seeing real wage growth for the first time in a long time. The effects of the Covid virus seem to be increasingly manageable, at least in the US. People are travelling, the schools are open and businesses are trying to balance productivity with employees who want to work fewer hours in the office and spend more time at home. There is some reason for optimism. Maybe a little less piling on?

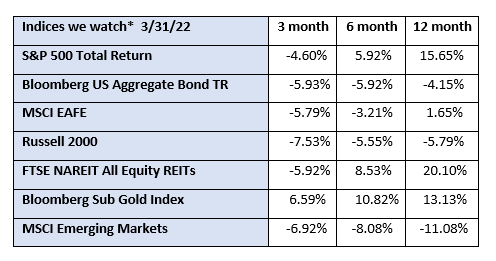

The figures in the chart above are not pretty. Large-cap US stocks were down, international stocks were down more, and small-cap US stocks were down even more. Rising interest rates caused the aggregate bond index to lose almost 6% last quarter. Real estate was down, even though housing prices and rents are increasing. The only bright spot was gold, and when gold is the only bright spot it doesn’t usually bode well, as it is still considered the safe haven of asset classes. It was not a good quarter, yet… it just feels like it should have been worse.

We are entering an interesting phase. Some of the forces at play are event driven and should correct themselves over time, such as the war in Ukraine and the Covid pandemic. The gradual unwinding of the Federal Reserve’s decade long easy money policy will be painful to go through, but it should hopefully end in an environment where an investment in a CD will generate enough of a return to make it a viable savings option. We have a ways to go, a long way, perhaps, but it is starting to feel like some of the weight is shifting in the pile.

*The index returns are drawn from Morningstar Advisor Workstation. Indexes are unmanaged and cannot be invested in directly by investors. MSCI EAFE NR USD-This Europe, Australasia, and Far East index is a market-capitalization-weighted index of 21 non-U.S., industrialized country indexes. S&P 500 TR USD – A market capitalization-weighted index composed of the 500 most widely held stocks whose assets and/or revenues are based in the US; it’s often used as a proxy for the stock market. TR (Total Return) indexes include daily reinvestment of dividends. Bloomberg US Agg Bond TR USD This index is composed of the BarCap Government/Credit Index, the Mortgage Backed Securities Index, and the Asset-Backed Securities Index. The returns we publish for the index are total returns, which includes the daily reinvestment of dividends. The constituents displayed for this index are from the following proxy: iShares Core US Aggregate Bond ETF. MSCI Emerging Markets IndexSM is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. Russell 2000 – Consists of the smallest 2000 companies in the Russell 3000 Index, representing approximately 7% of the Russell 3000 total market capitalization. The returns we publish for the index are total returns, which include reinvestment of dividends. The MSCI Emerging Markets (EM) IndexSM is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. As of May 2005 the MSCI Emerging Markets Index consisted of the following 26 emerging market country indices: Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Israel, Jordan, Korea, Malaysia, Mexico, Morocco, Pakistan, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, Turkey and Venezuela.. The FTSE NAREIT Equity REITs Index is an index of publicly traded REITs that own commercial property. All tax-qualifies REITs with common shares traded on the NYSE, AMSE or NASDAQ National Market List will be eligible. Additionally, each company must be valued at more than $100MM USD at the date of the annual review. Equity REITs include Diversified, Health Care, Self Storage, Industrial/Office, Residential, Retail, Lodging/Resorts and Specialty. They do not include Hybrid REITs, Mortgage Home Financing or Mortgage Commercial Financing REITs. Bloomberg Sub Gold TR USD Description unavailable. Formerly known as Dow Jones-UBS Gold Subindex (DJUBSGC), the index is a commodity group sub-index of the Bloomberg CI composed of futures contracts on Gold. It reflects the return of underlying commodity futures price movements only and is quoted in USD.